Rumours are rife that an Indian entrepreneur is close to completing a takeover of Blackburn Rovers football club in a deal worth between £35 and £45 million. Saurin Shah apparently hopes to establish strong marketing links with cricket’s Indian Premier League (IPL), where his uncle Niranjan Shah holds the post of vice-chairman. He considers Blackburn a perfect fit because of the town’s large Asian population, while India is regarded by many Premier League clubs as an area of huge potential growth, so such a partnership could bring a much-needed boost to Rovers’ commercial revenue.

It is far from certain that the deal will go through, first because Shah’s team is still conducting due diligence, and second because it is unclear how wealthy the little-known businessman really is. He may well have the funds, but up till now nobody seems to have heard of him in business circles. The only thing that Blackburn’s chairman, John Williams, would admit to is: “The situation is fluid, there is real interest and discussions continue.”

Long-suffering Blackburn fans have been down this road many times before. The club put up the “For Sale” sign three years ago, when they appointed Rothschilds as corporate advisors to find potential buyers, but so far the search for new investors has drawn a blank. The chairman has said that the owners are “in no hurry to sell”. You can say that again. Several parties have now looked at the books, but they have all ended up walking away.

"Chairman of the Board"

Back in 2007, there was some talk of South African billionaire Johann Rupert and NFL Miami Dolphins owner Wayne Huizenga joining forces for a bid, but nothing materialised. In January 2008, a US-based consortium lead by Lancashire-born Dan Williams was involved in several rounds of talks before withdrawing from the process. Later that year, JJB Sports owner Chris Ronnie was reported to be close to a takeover before pulling out of a bid and there was also the inevitable property tycoon, Nabeel Chowdery, who declared an interest before baulking at the valuation.

Obviously, anyone buying the club would need enough money for more than just the purchase price, whatever that is, as they would also need to repay any outstanding loans (currently £20 million), provide a transfer budget of at least £10 million for new players “to move to the next level” and fund ongoing losses. The club’s trustees would also “like to see a takeover funded with equity and not debt”, as they believe that any increase in external debt could “threaten the financial status of the club.” However, the owners would not need to finance a new stadium and they would be acquiring a club with modern facilities that is well established in the most lucrative league in the world.

Unsurprisingly, chairman John Williams agreed with this assessment, “the acquisition of Rovers as a Premier League club with relatively small debts presents a tremendous opportunity for the right person.” However, he sent out some slightly mixed messages, when he admitted, “I don’t really think anyone is going to buy into Blackburn Rovers looking for a return on their investment.” Nevertheless, the quest for investment continues, as “everyone knows suitable new ownership with new money coming into the club would be the answer.”

"Jack Walker and some TV pundit"

So what would an investor get for his money? A traditional family club very much in touch with its East Lancashire roots, Blackburn Rovers has a lot of history, having won the league three times and the FA Cup six times. The problem is that most of this is ancient history with two of the league wins coming before the First World War and all but one of the FA Cup triumphs coming in the 19th century. In fairness, they are also the only team to have won the Premier League since its inception in 1992 outside of Manchester United, Arsenal and Chelsea.

The Premiership victory in 1995 was the pinnacle of Blackburn’s rise during the Jack Walker era. “Uncle Jack” was a local businessman made good, who bought his hometown club in 1991 when they were languishing at the wrong end of the old Second Division, and spent big money (for the time) in order to improve their prospects. He broke the British transfer record twice on forwards Alan Shearer and Chris Sutton, who formed the so-called SAS (after the elite British special forces), which is ironic considering the club is now sending out an SOS for new money. It would not be too harsh to say that Jack Walker’s money bought Blackburn success, but expectations have had to be lowered since those halcyon days.

Since Jack Walker’s death in 2000, the club has been owned by the Jack Walker Settlement Trust, which is based in Jersey, where Walker was a tax exile. The Trust has invested well over £100 million, most notably converting £14 million of loans into share capital in 2006, followed by the conversion of £80 million preference shares into equity in 2007. They also provided annual funding of £3 million for six years, but the money has now all but dried up. In fact, in 2007/08 the trustees discontinued this support, arguing that there was no requirement to invest further, given the new TV deal, though they were persuaded to provide a £3 million loan for the 2008/09 campaign.

This limited financial support has impacted upon the club’s financial status, though it was always Walker’s wish that the club would become self-sufficient. To be fair, if we look at the club’s recent profit trend, they are more or less there, even though Walker could never have foreseen the explosion in transfer fees and wages (despite having to some extent lit the touch paper himself). At the level of operating profits, the total over the last five years is a small net loss of £1.6 million. The pre-tax losses (after player trading and interest) are higher, but the club should be praised for making profits in the last two years (£3 million in 2008 and £3.6 million in 2009), even though last season was boosted by high player sales, notably Roque Santa Cruz to Manchester City. They don’t have the financial backing of many other Premier League clubs, but it is evident that they are being run on sound business lines.

Like so many English clubs, their strategy is a simple one: to stay in the Premier League, so that they can continue to enjoy the financial benefits of the world’s richest league, in particular the vast television money. As Williams put it, “So long as we can preserve our PL status, the club is stable.” This is presumably why manager Sam Allardyce is always so keen to announce when Blackburn are mathematically safe from relegation.

"Happy days are here again"

This has resulted in a high-wire balancing act for the past ten years with any profits made being re-invested in the team, either as capital expenditure (transfer fees) or wages, leading to an apparently suicidal wages to turnover ratio of 91%. However, there is some method behind this madness, as they need this level of salaries to remain competitive. Williams argued, “I would term the wage bill as not reckless, but a calculated gamble, a true expression of our ambition.”

If they need to balance the books, they cover the shortfall by selling players, a policy that can be understood by examining the transfer activity last summer. In 2008/09, there was a hole in the P&L, because a lower league position than budgeted lead to less television income. The club (more than) compensated for this with the proceeds from the sale of Roque Santa Cruz with the balance being used to fund the purchases of Nikola Kalinic from Hajduk Split and Gael Givet from Marseille.

As the club then prepared budgets for the 2009/10 season, they were faced with the choice of reducing wages by 10% or gaining £4 million from player sales, which they achieved by selling Stephen Warnock to Aston Villa for £7 million, replacing the full-back with Pascal Chimbonda from Spurs for £3 million. Selling players to maintain operating expenses may not be everyone’s business model of choice, but it seems to just about work for Blackburn Rovers, where player trading has become the name of the game.

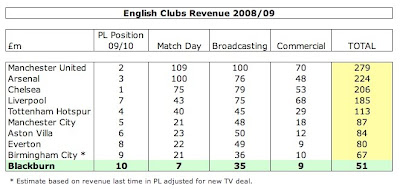

This policy has been born out of necessity, as Blackburn’s revenue is very low compared to other leading clubs in the Premier League. If we look at the revenue of the clubs who finished in the top ten positions in the 2008/09 season, Blackburn’s revenue of £51 million is easily the smallest of those clubs. OK, you would expect them to be significantly behind the so-called Big Four (Manchester United £279 million, Arsenal £224 million, Chelsea £206 million and Liverpool £185 million), but they are also earn a lot less than clubs like Aston Villa (£84 million) and Everton (£80 million), while even Birmingham City generate more income (£67 million).

The most startling difference comes from the match day revenue, where Blackburn receive less than £7 million a year. All the other clubs in the top ten earn a minimum of three times that amount with their near neighbours, Manchester United, pocketing over £100 million more. As John Williams explained with some justification, “attendance is the one area where we find it difficult to compete.” This is not overly surprising, if you consider that Blackburn is a “small, relatively impoverished town with a small fan base” (not my words, but the chairman’s), which has greatly suffered in the recession. The problem is not just that it’s a relatively small town, but it’s the fact that Blackburn is located very close to many other football clubs in the North West of England, so there is a limit on how successful the club can be in terms of attracting spectators.

Attendances of 23,500 in the 2008/09 season were among the smallest in the Premier League, only ahead of Bolton and Portsmouth, and were actually lower than four clubs in the Championship and one in League One (Leeds). This represented a 2% decline over the previous season’s crowd, though it is a fair bit higher than the nadir of 22,000 in 2004/05. This means that only 75% of the ground’s 31,400 capacity is being filled on average.

"David Dunn - local boy made good"

This provoked a campaign to “take back Ewood” with ticket prices being reduced by 25%, which means that Blackburn Rovers now have the cheapest season tickets in the Premier League at £224. Although some might argue that this is still too high a price to pay to watch any team coached by Big Sam, it has worked to the extent that attendances have increased and season ticket sales increased from 14,000 to 18,500, though overall gate receipts are still down. Blackburn’s pricing structure is now very similar to that of a Championship team, but the problem is that the club has Premier League expenses.

Similarly, commercial revenue of £9 million is also on the low side and has been declining over the last few years, though this is a bit misleading, as it has included some strange items in the past. Up until 2007/08, this was where Blackburn booked the annual £3 million funding from the Jack Walker Trust. The 2008 accounts contained a once-off settlement from Sports World International after the club took back responsibility for the retail operation, while the high commercial revenue in 2005 was boosted by £1.5 million compensation from Manchester City for securing the services of Mark Hughes and his management team. The current sponsor is Crown Paints, who replaced Bet24 in 2008, but they only pay £4-5 million for a three-year deal, while the shirt supplier is Umbro.

What really drive Blackburn’s turnover is television. Almost 70% of their total income comes from TV, which is only behind Wigan and Portsmouth in terms of Premier League clubs, even though their £35 million is nowhere near as much as the leading clubs earn, mainly due to the money those teams earn in the Champions League. Williams noted the “obvious effect on our business”, but was honest enough to admit that the club was “too heavily dependent on TV revenue.”

Blackburn’s record turnover of £56 million in 2008 was heavily influenced by the new broadcasting deal, which increased TV revenue from £24 million to £41 million (an rise of over 70%). Similarly, nearly all of the £5 million decrease in revenue in 2009 to £51 million was almost entirely due to the fall in TV revenue from £41 million to £35 million, because of the lower merit payment arising from a lower league position.

Most of the 2009 TV revenue (£34 million) came from the Premier League’s central distribution and we already know that the 2010 payment will be £7 million higher, largely because of Blackburn’s higher league position (10th compared to 15th) and more live TV appearances. This highlights the importance of final league place, each of which is worth £800,000, to a club like Blackburn, especially as this is budgeted “aggressively”.

"Paul Ince - no longer the guv'nor"

A key part of Blackburn’s strategic planning is to anticipate higher revenue from the new broadcasting deals. Happily for Blackburn (and others), the central payments from the next three-year deal, which kicks off in the 2010/11 season, will climb by about a third, largely thanks to the increase in overseas rights, so they can anticipate another £10 million in revenue. However, woe betide them if this gravy train stops or even slows down.

This is why the club is so nervous of relegation, which would have severe repercussions for their financial well-being. Williams acknowledged that “the model would come under threat”, if they lost their Premier League status. This was the key factor behind the decision to sack Paul Ince in December 2008 after just six months in charge, as they considered that this was the club’s best chance to avoid the nightmare scenario.

The parachute payments paid to clubs dropping out of the Premier league have been increased to £48 million (£16 million in each of the first two years, £8 million in each of years three and four), but this would still represent a drastic reduction for Blackburn. They can expect around £50 million revenue from the Premier League next season, so they would have to confront a £34 million reduction in their total revenue. This would effectively mean that they could not meet their payroll, so would have to offload players, making it more difficult to be promoted back into the top division – a vicious circle. Inevitably, some clubs gamble on getting back after one season, keeping most of their players and taking a financial hit that season, but they are taking a big risk.

Of course, if a football club wishes to cut back on costs, there is realistically only one place they can go – the playing squad. But Blackburn are on the horns of a dilemma: either they cut wages and increase the chances of relegation (with all the revenue implications); or they keep wages high and run the risk of financial ruin. In fact, their wages have been on an upward trend, rising from £31 million in 2005 to £46 million in 2009 (an increase of nearly 50%). Indeed, salaries grew by a worrying 16% in the last season alone, “reflecting the cost of attracting and retaining players and the market within the Premier League generally.” Effectively, Blackburn and other clubs have channeled the increases in TV revenue directly into the players’ bank accounts.

The increase in wages is not primarily due to transfer activity, but improving contracts for existing players. Again, this is a conscious decision, where the club has accepted the additional cost in order to secure their players, so that they may be profitably sold at a later date, which is an important element of Blackburn’s business model.

"Roque Santa Cruz - a model professional"

However, this has produced what the club itself describes as an “uncomfortable ratio of wages to turnover” of 91%, which is, needless to say, one of the worst in the Premier League. The problem is not so much the absolute level of the wage bill – it’s only the 12th highest in the Premier League – but the disproportionately low turnover, which is very difficult to address. There is a clear correlation between a club’s wage bill and its success on the pitch, so Blackburn are unwilling to reduce their wages, which means that they have to invest a greater proportion of their income than their competitors.

If they wanted to lower their wages to turnover ratio to a more reasonable 60%, they would have to cut their wage bill by a third from £46 million to £31 million. Alternatively, they would have to grow revenue by a half from £51 million to £77 million, which would be ambitious to say the least. There is some light at the end of the tunnel with the improved TV deals, but the other avenues have limited growth prospects – unless someone like Saurin Shah really can greatly expand their marketing reach.

Obviously, player trading can be another source of revenue, but up until last season Blackburn Rovers have essentially been a trading club, balancing sales and purchases. Last year was exceptional with the sales of Roque Santa Cruz and David Bentley contributing towards a large surplus on transfer movements and a £19 million profit on player sales. This approach was summarised by Williams, “We can’t go out and spend £5 million on a player who is not good enough. That would kill us, because our finances are so finely balanced.” However, he was at pains to emphasise the difference between a selling club, which is one that has to sell, and a trading club (like Blackburn), which is one that cannot afford to buy, but does not have to sell. Having said that, he accepted that without external funding, Blackburn could easily become a selling club in the truest sense of the word.

Television revenue again plays a part in their thinking, as they try to buy players the year before a new TV deal kicks in on the assumption that they will be more expensive 12 months later. This helps to justify last year’s high wages to turnover ratio as a rational decision to buy players at the right price, making sure the club survived in the Premier League, in order to benefit from the extra income. They have also looked at recruiting young, cheaper players, not just into the academy, but ones who can rapidly progress into the first team.

As you would expect from this cautious approach to the transfer market, player amortisation, which is such a big expense for many clubs, is relatively low for Blackburn at just £8 million. To place that into context, Chelsea booked £49 million for this expense last year, while even the famously parsimonious Everton recorded £13 million.

"A snarling, fat-headed beast and Roar the Lion"

The club’s debt also seems relatively low with bank loans constant at around £14 million, though these will increase to £20 million by the end of 2009/10, a level that is described as “manageable, but cannot be allowed to increase further.” In fact, the total debt is already £20 million after including the £6 million owed to the parent undertaking, i.e. the Jack Walker Trust. These loans are interest-free, unlike the bank loans, which carry interest at LIBOR plus 3.25%.

The real issue with the debt is the repayment schedule. The bank loans need to be repaid by May 2012 – in equal installments according to the accounts, implying £4.8 million a year. The shareholder loans required £1 million to be repaid in both November 2009 and November 2010 with the timing for the remaining £4 million not agreed, but expected to follow a similar schedule. This all means that within the next two years the club must definitely find £20 million for the bank loans and potentially another £6 million for the Trust, though the owners may be more flexible on the phasing of their repayments.

The club believes that the debt level is acceptable, given the value of its assets, so what do they have to support the balances they owe? First off, they own their stadium and 50 acres of freehold land, which are included in the accounts at £39 million, but may well be worth more in the real world. Ewood Park was in some ways the prototype for today’s modern, all-seater stadiums. The directors have valued the playing squad at £47 million – much higher than the net book value of £13 million in the books. This provides solid under-pinning of the debt, but does not help to release cash to make repayments, unless players are sold, hence the club’s desire to secure new money from investors.

"El Hadji Diouf - spitting mad"

In the meantime, Blackburn Rovers will have to soldier on, struggling with their limited turnover. With some justification, their fans may feel that they are not operating on a level playing field, but others would be quick to remind them that not so long ago they were the beneficiaries of Jack Walker’s generosity. Despite the financial constraints, they have performed creditably, finishing tenth and reaching the Carling Cup semi-final last season, even though their uncompromising brand of football is not everyone’s cup of tea.

On the one hand, Blackburn have to be admired for their efforts to survive in the Premier League, while balancing the books, but on the other hand, the club has admitted that it is “punching above its weight”, and you do wonder what would happen to them (and others of the same ilk) if the TV funds were to dry up.

{kind=link}