There’s no doubt that the 2009/10 season was a triumphant one for FC Internazionale, better known as Inter, as they became the first Italian team to complete the treble by winning the scudetto, the Coppa Italia and the Champions League in a single year. In fact, Inter have been the dominant force in Italian football ever since the Calciopoli scandal in 2006, winning five league titles in a row, the first time this has been done since Juventus achieved the feat in the 30s.

This recent success must taste all the sweeter to Inter fans, as it follows a lengthy period of failure and disappointment. After winning the league in 1989, the nerazzurri endured 17 long years without taking the Serie A title, which was made even worse by their arch-rivals Milan sweeping all before them, but now the boot is well and truly on the other foot.

The victory over Bayern Munich in Madrid to secure the Champions League trophy represented the high point of Massimo Moratti’s reign as Inter’s president. Moratti is the fourth son of Angelo Moratti, who had been Inter’s owner and president during the club’s golden age from 1955 to 1968, when the team twice won the European Cup under the legendary Helenio Herrera. The current president took over the club in 1995, determined to restore Inter to its former heights, and he has spent a fortune attempting to fulfill that ambition.

"Mourinho and Moratti - the happy couple"

Using money earned from the family’s stake in Saras, an oil refiner, Moratti has repeatedly funded lavish spending sprees, twice breaking the world transfer record when buying Ronaldo from Barcelona and Christian Vieri from Lazio, but also splashing out on the likes of Roberto Baggio, Hernan Crespo and Juan Sebastian Veron.

Even so, Moratti has an impatient, not to say ruthless, side and he has gone through 14 managers in 15 years in his quest for honours, sacking many big names like the popular Luigi Simoni, Marcello Lippi, Hector Cuper and Roberto Mancini. When il Mancio was given the boot, Moratti explained that this was for the benefit of the club, “I intervened because I thought it was necessary … in the interests of Inter.”

In the past, Moratti has been criticised by many Inter fans, but he can hardly be accused of not putting his money where his mouth is, as he has spent around a billion Euros on delivering the dream. The president’s support has been an absolutely essential part of the club’s success, for the reality is that Inter do not make profits. Instead, they lose money. In fact, they lose a lot of money.

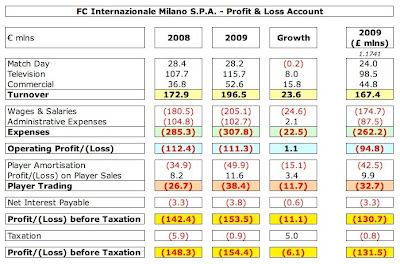

The last available accounts are for the year ending 30 June 2009 and these report an enormous loss of €154 million (£132 million). Just a blip? Not a bit of it – the previous year’s loss was very nearly as bad at €148 million and the 2007 loss was even worse at €208 million. That gives a cumulative loss of €509 million in just three years – over half a billion!

In fact, the profit and loss account has been a tale of woe throughout Moratti’s presidency. Even the reported loss of “only” €31 million in 2006 was boosted by the sale of Inter’s brand to a subsidiary, so it was really a €181 million loss after intra-group transactions had been eliminated. There were suggestions that some of the accounting entries at that time, including inflated transfer fees to secure fictitious capital gains, were a little too creative, leading to talk of a financial investigation.

There has been much discussion in the English media about gigantic losses at Chelsea, Manchester City and Barcelona, but the scale of Inter’s losses is breathtaking. According to the respected Il Sole 24 Ore (the Italian equivalent of the Financial Times), Inter’s combined losses during Moratti’s era amount to €1.15 billion with about €730 million of this being covered by the president.

"The immovable object"

What is particularly worrying is that Inter has produced such large losses during these highly successful years, but maybe the cause and effect are the other way round? In other words, all this silverware would not have arrived without all this expenditure. Moratti himself seems to have no doubts, advising the club’s Annual General Meeting, “The considerable loss is justified to keep our team at the top level worldwide.”

To put this into context, Tuttosport (admittedly a newspaper based in Turin) compared the relative achievements of Inter and Juventus last season. From a financial perspective, Inter’s €154 million loss was €161 million worse than the €7 million profit that Juventus made. On the pitch, Inter finished ten points ahead of Juventus, so that works out at €16 million a point. Obviously, it’s not quite as simple as that, but you can understand their, er, point.

In fairness to Inter, if last year’s accounts had been extended by one month to the end of July, the reported loss would have been €56 million lower, as the highly profitable sales of Zlatan Ibrahimovic and Maxwell to Barcelona would have been included. Having said that, the loss would have still been a thumping great €98 million, which is nothing to write home about.

"OK, he is a bit special"

Clearly, money alone can’t buy you success (or love) and we should give Inter a lot of credit for their sporting achievements. The self-proclaimed “special one”, Jose Mourinho, built a formidable unit, largely based on the uncompromising defence of Lucio and Walter Samuel, but also finding space for talents like the mercurial Wesley Sneijder and the goal scorer par excellence, Diego Milito. Although Mourinho is not everyone’s cup of tea (“I don’t like Italian football and it doesn’t like me”), he is a winning coach and he duly delivered a winning team, before moving on to Real Madrid. Finally Moratti had allowed his coaches a few seasons to build a squad and the positive results were there for all to see.

You may justifiably be wondering how one of Europe’s major clubs, with such a rich football tradition and such a large fan base, could possibly be struggling financially. The reasons start with their revenue.

On the face of it, Inter’s revenue is not too bad at €197 million (£167 million), which places them 9th in the Deloitte Money League, ahead of their neighbours Milan for the first time, and also represents €24 million (14%) growth over the previous year. However, problems begin to emerge when we take a closer look. Although Inter’s income is in line with the other top Italian clubs, it a long way short of their natural competitors abroad. For example, Manchester United earn £111 million more with £278 million, while the Spanish giants, Real Madrid and Barcelona, generate well over £300 million, which is around twice as much revenue as Inter. This makes it difficult to compete, especially when that difference in turnover is every year.

The reasons for the shortfall are evident, as there are striking flaws in Inter’s business model. Among the top ten clubs listed in the Money league, Inter has the lowest commercial revenue of £45 million and the second lowest match day revenue of just £24 million. These are obvious financial weaknesses that the club needs to address.

At this stage, eagle-eyed observers will have noted that the revenue figures in my analysis are different from those quoted by the club. In order to be consistent with other clubs, I have used the Deloitte definition, so have excluded the following: (a) gate receipts given to visiting clubs €3.6 million; (b) TV income given to visiting clubs €17.8 million; (c) profit from player sales €11.6 million; (d) increase in asset values €3.1 million. Adding the total adjustments of €36.1 million to the Money League revenue of €196.5 million gives the €232.6 million revenue reported by Inter.

OK, that’s enough technical talk, let’s look at how Inter make their money.

Like all the big Italian clubs, the majority of the club’s revenue (59%) comes from television with €116 million, which is €8 million more than 2008. Inter’s broadcasting deal with Mediaset, extended until the end of 2009/10, earned them around €100 million gross before payments to visiting teams, which represents a significant uplift on the previous agreement with Sky Italia.

However, the growth of the Champions League has also been a key driver in the increased TV revenue with the central distributions in 2008/09 being worth €28 million. After Inter’s Champions League victory, the 2009/10 distribution will be significantly higher, as UEFA has confirmed the payment as €49 million (€7m for participation, €22 million for winning it and €20 million from the market pool).

Great stuff, but there are clouds on the horizon, starting with a price war between Rupert Murdoch’s Sky Italia and Silvio Berlusconi’s Mediaset that may ultimately impact the fees paid for the Serie A TV rights. That outcome is by no means certain, but what is definitely happening is a move to collective selling of TV rights from 2010/11.

Currently, teams like Inter sell their TV rights on an individual basis, so intuitively we would expect their television revenue to reduce due to the more equal distribution of revenue amongst all clubs. However, early projections indicate only a small decrease for Inter (€1 million) for a couple of reasons. First, the total money guaranteed by exclusive media rights partner Infront Sports will be approximately 20% higher than before at over €1 billion a year. Second, the complicated distribution formula favours the big clubs: 40% equal share; 30% based on past results (5% last season, 15% last 5 years, 10% since 1946); and 30% based on catchment area/number of fans.

"We are the champions!"

Of course, the new arrangement will mean that mid-ranking clubs earn more TV money and it will also restrict the growth potential for the larger clubs, unless those responsible for Liga Calcio can greatly increase the fees received for overseas rights, which currently lag way behind the Premier League (in particular) and La Liga. That may seem ridiculous at this time, but sport business expert Simon Chadwick believes that, “leagues on the continent will inevitably catch up with the Premier League.” We shall see – there’s certainly room for growth.

The same thing could also be said about Inter’s commercial revenue. Even after a substantial €16 million (43%) rise in 2009 to €53 million, it is still on the low side for a club of Inter’s stature. As a comparison, the opponents they defeated in the Champions League final, Bayern Munich, earned €159 million from this revenue stream last year. On the one hand, Inter have benefited from very long-term relationships with commercial partners, but on the other hand, this may have prevented them from taking up more lucrative opportunities elsewhere. Pirelli have been Inter’s shirt sponsor since 1995 and are also a minority shareholder in the club, which may help explain why they only pay €9.3 million a year. Similarly, kit supplier Nike have been partners since 1998 and pay €18.1 million a year for the privilege.

"You can put your shirt on us"

These deals do not seem particularly good, considering that we are talking about the winners of the Champions League. As an example, Liverpool, who have not even qualified for the Champions League, recently signed a shirt sponsorship deal with Standard Chartered at €24 million a year. The same Nike that gives Inter just €18 million somehow pays €30 million to Barcelona as kit supplier. And it’s not just foreign clubs that negotiate better deals, as Milan’s sponsorship deal with Emirates is also higher at €12 million a season. Even Juventus’ deal with BetClic is only a little lower at €8 million, even though they will only display their wares in the Europa League this season - and that's just for the home shirt.

More optimistically, the next accounts should show an improvement with La Gazzetta dello Sport estimating that the Champions League win should result in an additional €6 million from sponsors, presumably due to success-based clauses in the contracts, and €8 million from merchandise sales. Nevertheless, it is clear that the commercial department needs to pull its collective finger out. Despite pre-season tours to China and the US, the club has not really managed to develop a global brand that resonates in overseas markets.

Even though marketing revenue could be higher, Inter’s real Achilles’ Heel is match day revenue, which is embarrassingly low at €28 million. In fairness, this is a common problem for all Italian clubs with Milan earning €33 million and Juventus only €17 million. However, this is considerably less than other major European clubs. Despite attracting average attendances of 55,000, Inter’s revenue per home match was only €1.1 million, compared to the top six Money League clubs who all generated at least €2.6 million. That’s a massive difference to make up.

"Breaking new ground?"

This is why Inter have been exploring plans for moving to a new stadium, possibly bringing to an end the famous ground sharing arrangement with Milan. San Siro is a wonderful old ground, but it is owned by the local council, which is very “detrimental” to Inter’s revenues, according to managing director Ernesto Paolillo. Not only does the club have to pay rent and maintenance of around €13 million a year, but it misses out on many opportunities through not owning the stadium.

The proposed ground would only be ready by 2014, holding 60,000 spectators, but importantly it would include 150 VIP boxes and 5,000 corporate seats, which could significantly enhance match day revenue. As a comparison, Arsenal make 35% of their match day revenue from just 9,000 premium seats at the Emirates. A new stadium would require a huge initial outlay (estimated at around €400 million) and is not necessarily a magic bullet, given that it would be difficult to raise ticket prices in an economic recession, but it could have a dramatically beneficial impact on Inter’s revenue. You only have to look at how Arsenal’s revenue overtook Inter’s in 2007 – the first year that the Emirates became operational – to appreciate the size of the prize.

If the club owned the stadium, it would also keep the receipts from non-sporting events like rock concerts in the summer (the likes of U2, Springsteen and the Rolling Stones have played San Siro), while it could also coin it from restaurants, parking, club shop, museum, etc. Finally, money would surely be on the table for naming rights (the Pirelli stadium, anyone?), which is more acceptable to fans when we’re talking about a new development, rather than renaming an existing ground.

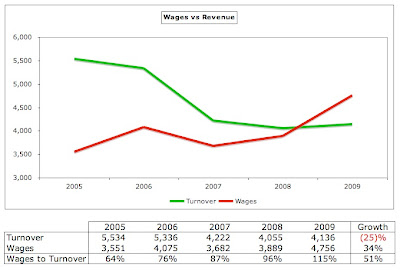

All in all, the revenue is not great, but it’s not too bad. Inter’s real problem lies in the costs of €358 million (expenses €308 million plus player amortisation €50 million), which are far too high for their turnover of €197 million. They’re in the same range as Barcelona’s 2008/09 costs of €362 million, the only difference being that Barcelona’s revenue was much higher at €364 million. Basically, the impressive 2009 revenue growth of €24 million has been wiped out (and then some) by cost growth of €38 million, which is entirely down to staff costs: salaries €25 million and player amortisation €15 million.

The total wage bill stands at a jaw-dropping €205 million, which produces a wages to turnover ratio of 104%, way beyond any common sense let alone financial prudence. There has been a significant increase in wages over the last two years, rising from €162 million in 2007. In the accounts the club explains last year’s growth as being due to new players and an increase in bonus payments. The first part is accurate, as the players’ headcount increased by 6, but the second part is nonsense, as the bonus payments actually fell from €28 million to €25 million. Whatever. The fact is that Inter’s payroll is much higher than other Italian clubs: Milan paid €177 million, while the Juventus wage bill was only €130 million. Inter even paid more out in salaries than those well-known big spenders Real Madrid (€187 million), for heaven’s sake.

"Zlat's the way I like it"

However, that was then, this is now. The four highest-earning individuals at Inter in 2008/09 (Mourinho, Ibrahimovic, Adriano and Patrick Vieira) have all left the club as a sign of things to come, leaving only Samuel Eto’o in the latest list of the top 50 highest paid footballers. After the latest financial losses were announced, Moratti said that the staff costs would be cut. In particular, he spoke of a fundamental change in the structure of new salary contracts with a significantly lower guaranteed element plus higher variable payments linked to success on the pitch.

There was also a steep increase last year in player amortisation from €35 million to €50 million. That’s a lot, though it’s still on the low side compared to clubs known for being big spenders in the transfer market: Real Madrid €64 million, Chelsea €59 million and Barcelona €54 million (though this is up to €71 million in the 2009/10 accounts). Remember that amortisation is the annual cost of writing-down a player’s purchase price. For example, Christian Chivu was signed for €16 million on a five-year contract, but his transfer is only reflected in the profit and loss account via amortisation, which is booked evenly over the life of his contract, i.e. €3.2 million a year (€16 million divided by five years). Thus, the total cost of player purchases is not immediately reflected in the expenses, but increased transfer spend will ultimately result in higher amortisation.

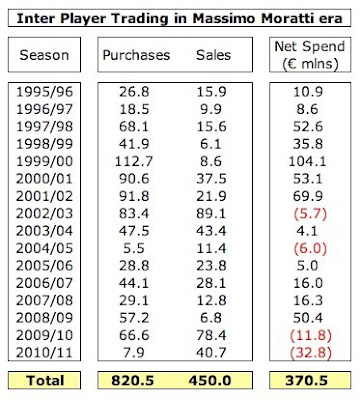

Inter’s relatively low amortisation therefore suggests that their spending in the transfer market has slowed down and that is indeed the case. In fact, Inter have net receipts in the last two years of €45 million. This is very different to the majority of the Moratti era, in which Inter wrote the large cheques. In the 15 years since Moratti took the helm, Inter have spent €821 million on buying new players, though they have recouped over half of that, leaving a net spend of €371 million. While acknowledging that transfer fees are sometimes open to question (e.g. the fee quoted for the Ibrahimovic transfer in Inter’s accounts is different to that quoted on Barcelona’s website), there can be no argument that Inter have consistently splashed the cash.

Until now, that is, when they are giving the impression of being a selling club. They made a €12 million profit on player sales in 2008/09, largely from transferring Robert Acquafresca to Genoa and Pele (not that one) to Porto, but since then they have really done some business. After hearing that Bayern Munich had slapped a €70 million price tag on Franck Ribery, Moratti risked ridicule by saying that in that case Ibrahimovic was worth €90 million, but he was more or less vindicated when he sold the tall striker to Barcelona for €46 million plus Eto’o (estimated value €20 million) and the loan of Alex Hleb. This summer, Moratti has already realised €27 million by selling the talented, but temperamental, Mario Balotelli to Manchester City and there is talk that he may yet raise a similar sum from the sale of Brazilian full back Maicon.

In any case, player purchases are one of the reasons for Inter’s high debt levels. Actually, that statement is open to debate. In the red corner, we find our old friend, “Spain’s foremost football finance expert”, Jose Maria Gay de Liebana from the University of Barcelona, who included Inter in a list of football clubs with high debt, quoting a figure of €432 million. He certainly convinced the UEFA president Michel Platini, who also described Inter as a club steeped in debt. In the blue (and black) corner, Inter’s managing director Ernesto Paolillo has responded that Platini’s claims are excessive and mistaken: “Inter are not in debt with the banks.”

So who’s right? Actually, they’re both wrong. The Professor’s figure is for total liabilities, thus including amounts owed to trade creditors and employees, and is clearly over-stated. However, Paolillo’s claim is also palpably incorrect, as the accounts include €48 million owed to banks – not an enormous sum, but clearly more than zero.

The most accurate definition of net debt is probably the one provided by UEFA, which includes amounts owed to and from other football clubs, and this would mean total net debt for Inter of €129 million. Not great, but far from terrible.

"It's been a good year for Diego's"

In Inter’s case, paying transfer fees in stages is a significant part of their business model: they owe an incredible €99 million to other clubs, up from €62 million the year before. The largest debt is €28 million to Genoa for Milito, but other clubs waiting patiently to be paid appreciable sums include Porto €17 million, Roma €15 million, Portsmouth €9 million, Cagliari €8 million, Ternana €7 million and Cittadella €5 million.

In fairness, this transfer activity has produced €158 million of intangible assets (player values) on the books, but their market worth is much higher - €335 million per Transfermarkt.

Also, much of Inter’s “debt” is internal with €113 million owed to Group subsidiaries, which means that it’s money effectively owed to Moratti.

Having said that, we probably should not gloss over Inter’s payables of €432 million, which account for 23% of the total liabilities in Serie A. The only other club with a similar level of liabilities in Italy is Milan €364 million (19%), while the next highest is Lazio €129 million (7%). However, Inter’s figure is still a lot less than Barcelona €552 million and, especially, Real Madrid €683 million.

"Payback time"

But how is it possible for Inter to have relatively low levels of debt, given their horrendous losses?

Step forward, Signor Moratti. As Paolillo explained, “Inter, like many Italian teams, has had negative balances, but has always covered itself with capital made available by the club’s owners.” That is why the president has been such an important figure in Inter’s success. Without his generosity, there’s no way Inter would have been able to recruit the calibre of players good enough to win the Champions League. For example, Moratti injected €70 million of capital into FC Internazionale Milano S.p.A. after the last results to cover the losses, which was on top of €50 million paid in at various stages of the year. That brings the total capital paid out of Moratti’s pockets in his time as president to around three-quarters of a billion Euros. Wow.

However, this approach will not work in the future, as Inter are faced with the new challenge of UEFA’s Financial Fair Play Regulations, which will ultimately exclude from European competitions those clubs that fail to live within their means, i.e. make a profit. These will be implemented in the 2013/14 season, though the monitoring period will cover the preceding two reporting periods, 2011/12 and 2012/13, so clubs like Inter are under pressure to rapidly eradicate their losses.

"Your debt should be this small"

Wealthy owners will be allowed to absorb aggregate losses of €45 million over three years for the first two monitoring periods, so long as they are willing to cover the club’s losses by making equity contributions. The maximum permitted loss then falls to €30 million from 2015/16 and will be further reduced from 2018/19 (to an unspecified amount). However, it is clear that Inter have a long way to go to get close to this “acceptable deviation”, let alone break-even.

Paolillo admitted that Platini’s criticisms of Inter might be valid concerning the club’s “self-sufficiency”, and UEFA’s president was quick to point out: “It's mainly the owners that asked us to do something - Roman Abramovich, Silvio Berlusconi and Massimo Moratti. They do not want to fork out from their pockets any more.” Indeed, Moratti has promised, “The company's philosophy for the next two years is to have a healthy balance sheet, so we will do what is necessary to achieve this.” Paolillo confirmed Inter’s willingness to tackle the losses, “'We will be ready to meet all the standards set by UEFA and we are working on various fronts. That means cutting costs and increasing revenues.”

"Money's too tight to mention"

This heralds a new period of austerity at Inter, as the club turns over a new leaf. Paolillo has warned Inter fans that “the old times are over, as football is close to collapse.” Marcel Vulpis, the professor of sport marketing at Milan’s Bocconi University, observed, “Moratti spent hundreds of millions for ten years before his team managed to win its first title. Now the era of Moratti the big spender is over.”

Actually, UEFA’s financial initiative may be quite timely for Moratti, as his company, Saras, appears to be facing a fair few challenges of its own at the moment, having made a loss of €55 million in 2009. This meant that it did not pay a dividend, which has been Moratti family’s largest source of income (over €280 million in the previous three years). Saras also had to issue a €250 million bond in order to raise funds.

That’s the problem when a club relies on a benefactor, even one who has been so munificent over such a long period. Such a model falters if the owner gets into financial difficulties, but can also suffer if there are legal issues, illness, loss of interest, etc. In a dynasty like the Morattis, it is also legitimate to ask whether his children will share his love for Inter and want to follow in his footsteps. Fortunately for Inter fans, both his sons, Angelo Mario and Giovanni (known as Gigio), seem to share his passion for the football club.

"Super Mario - up, up and away"

That’s future music, but can the club realistically achieve the stated aim of a balanced budget in two years? The accounts talk of improvement in the figures in 2009/10, largely due to the player sales, which have the double whammy of raising cash (€56 million last summer) and taking players off the wage bill. There will also definitely be an increase in the revenue from the Champions League win: guaranteed €21 million more from UEFA’s central payments, plus an estimated €14 million from commercial deals. I have seen some estimates of net losses between €70-90 million next year, which I think is a realistic objective.

For 2010/11, Inter will still be benefiting from the Champions League, as this accounting year will include the receipts from the UEFA Super Cup (€4 million) and the FIFA Club World Cup (€8 million), but they would need to repeat their victory in Madrid to maintain their TV revenue. You would also hope that there would be an indirect benefit, as winning sporting teams hold major appeal for sponsors. Finally, transfers will also boost the books with Balotelli’s sale plus the €10 million compensation paid by Real Madrid to secure Mourinho’s services being added to the pot. However, it is questionable whether Inter fans will accept a financial strategy that involves the club selling un campione every summer. This is not really a sustainable model for a top club.

"Will he be laughing in a few months?"

Inter’s challenge is made all the more difficult by the underlying problems in Italian football. Regarded as the place to be in the 80s, Serie A has been experiencing a crisis of confidence in the last few years, being confronted by crumbling infrastructure, falling attendances, outbreaks of hooliganism and isolated incidents of racial abuse. It’s almost as if there has been an inferiority complex against the Premier League and La Liga, which is understandable off the pitch, but somewhat puzzling on the field of play, given that Italy has produced three Champions League winners in the last eight years, one more than both the other leagues.

Whatever the future holds, one thing is clear: Inter can no longer afford to win at all costs. Rafa Benitez, the new head coach, faces a tough battle to repeat last season’s spectacular success, given the club’s financial constraints. Jose Mourinho was always going to be a daunting act to follow, but Benitez may have to do it on a shoestring budget.

{kind=link}

{kind=link}