Last week was going so well for Arsenal fans. First, their youthful team thrashed North London neighbours, Spurs, in a glorious performance at White Hart Lane, driven forward by an inspirational display from young tyro Jack Wilshere, the poster boy for Arsenal’s strategy of developing players from their academy. Then, away from the pitch, the board announced a sparkling set of financial results that confirmed their status as the best-run club in the Premier League.

However, pride comes before a fall and the home defeat against newly promoted West Bromwich Albion brought everyone back to earth with a bang. Here we go again was the refrain, closely followed by the obvious question of why the club does not invest some of this wealth in more experienced players to provide a stronger spine to the dazzling, but fragile, youngsters.

It’s certainly not due to lack of funds when you look at Arsenal’s results for the year ended 31 May 2010. The headline figures are quite superb with revenue of £380 million (2009 £313 million) and profit before tax of £56 million (2009 £46 million) both setting new record highs for the club. The PBT was up a notable 23%, but after some long-running issues with the taxman were resolved, the profit after tax was bizarrely even higher at £61 million, an incredible 73% higher than the previous year’s profit of £35 million.

"We do want his sort"

Impressive stuff, but the “most pleasing aspect of these results” for the chairman, Peter Hill-Wood, was that the returns generated in the property business allowed the club to repay £130 million of bank loans, significantly reducing the net debt from just under £300 million to £136 million, including massive cash balances of £128 million. This means that the property business is now debt-free, so any further sales will generate surplus cash. Given the risks and uncertainty arising from the downturn in the property market, that’s a simply stunning achievement.

As chief executive Ivan Gazidis observed, with commendable understatement, these financial results are “very healthy”.

To place this into context, only five Premier League clubs (including Arsenal) were profitable last year. In the traditional Big Four, only Manchester United also reported a profit, but this was much lower at £22 million and would have been a large loss without the £80 million they made by selling Cristiano Ronaldo to Real Madrid. Chelsea and Liverpool registered thumping great losses of £47 million and £55 million respectively, but Manchester City made them look like amateurs with their £93 million deficit. Ironically, the closest club to Arsenal’s level of profits is the one closest to them geographically, as Tottenham Hotspur made a £33 million profit, though this was also boosted by £57 million profit on player sales (Berbatov and Keane). Indeed, Spurs’ more recent half-year results showed an £8 million loss.

I can already hear people complaining that this is an unfair comparison, as Arsenal have benefited from property development, which is true, but it’s not quite as meaningful as some may believe. Yes, there was an enormous increase in property revenue from £88 million to £157 million, but this was almost matched by the growth in expenses, so the profit from property “only” increased from £6 million to £11 million. Don’t get me wrong, that profit is still better than a kick in the face, but it’s a lot smaller than the £45 million football profit. In other words, it’s still football that’s driving the business (though sometimes it may feel like the other way round).

Having said that, we can now anticipate some hefty windfall gains from property sales in terms of surplus cash, so we can say with some assurance that the club’s calculated gamble on its property development strategy has paid off. Nevertheless, it would not be a good idea to become over-reliant on bricks and mortar and Gazidis duly introduced a note of caution, “the profits from property are temporary and we need to make sure that in the longer term costs remain at a level which can be paid from our football revenues.”

A very astute comment, given that operating profit for the football business actually fell by a third (£10 million) from £30 million to £20 million. Revenue slightly decreased by £2 million, as a solid increase in television money failed to compensate for lower match day income arising from fewer home games and a reduction in commercial revenue attributed to the “recessionary climate.” At the same time, expenses rose £8 million, which was almost entirely due to higher wages.

"Na-Na-Na-Na-Nasri"

Fortunately, the football operating profit was boosted by £38 million made on player sales (up from £23 million the year before), though it was then reduced by £14 million of interest payments, giving £45 million pre-tax profit, which was £5 million higher than the previous year.

However, it is clear that the only reason that the football segment increased its profit year-on-year was that £15 million growth in profit on player sales, which is not something that you would expect (or indeed wish) to be repeated every year.

Let’s be very clear about this: even without any player sales, football would still be profitable – but only just at £7 million. Hence, the concerns about whether the football revenue will be enough to cover costs in the future, though, as we shall see later, there is one very obvious opportunity for revenue growth, namely commercial revenue.

Of course, most football chairman would give their right arm for such profits. In fact, they’ve probably been casting an envious eye on Arsenal’s ability to make money for many years, given that the last time that Arsenal reported a loss was eight years ago, way back in 2002, while total profits have been rising ever since the move to the Emirates: 2007 £6 million, 2008 £37 million, 2009 £46 million and 2010 £56 million.

Even the relatively low 2007 profit would have been much higher, if it were not for £21 million of exceptional costs incurred to refinance the stadium debt, which was actually a very good move, as it has resulted in a £12 million reduction in annual interest payments ever since. In the last three years alone, Arsenal have produced combined pre-tax profits of £138 million – an astonishing figure in the world of football, which is more accustomed to turning billionaires into millionaires.

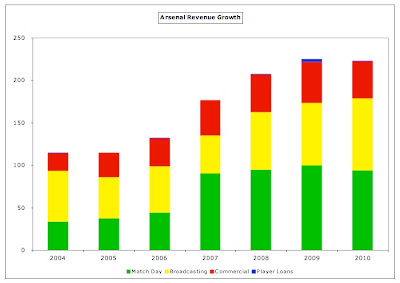

Profits from the property business are virtually unchanged since 2005, so the club’s profit growth has been very largely driven by tremendous revenue growth on the football side. In fact, this revenue has just about doubled in the last five years from £115 million to £223 million. This is second only to Manchester United among English clubs (£279 million) and placed Arsenal fifth in last year’s Deloittes Money League (based on 2008/09 results). Given the flat revenue in 2010, they will remain in that position when the next Money League is published. However, we should acknowledge that revenue has increased this year at both Real Madrid (to £375 million) and Barcelona (to £330 million). Of course, never was the old saying that “revenue is vanity, profit is sanity” more appropriate, as Barcelona’s huge turnover did not prevent them from making a gigantic £68 million loss and Real Madrid’s £22 million profit was a lot lower than Arsenal’s £45 million.

However, as the legendary investor Warren Buffett advised, “a rising tide floats all boats”, so it might just be that all football clubs have experienced similar revenue growth. In other words, Arsenal’s revenue growth might not be down to their own genius, but just due to the extra money pouring into football. “Up to a point, Lord Copper”, as Evelyn Waugh once memorably wrote, given that the big four clubs in England have all significantly increased their revenue in this period. However, the figures do show that Arsenal have outperformed their peers. They have overtaken Chelsea’s revenue, even during a period of sustained success for West London’s nouveaux riches, widened the difference with Liverpool and slightly closed the gap with Manchester United.

Unlike the vast majority of other clubs, the principal reason for Arsenal’s revenue growth is not television, but match day income from the new stadium. This can be clearly seen in 2007, the first season at the Emirates, when there was a step change in this revenue stream from £44 million to £90 million. This doubling of gate receipts has had a massive impact on Arsenal’s total revenue and justifies the board’s courageous decision to leave Highbury.

With a capacity of just over 60,000, the Emirates can accommodate 22,000 more fans than that famous old ground, which is great for those supporters, not to mention the bean counters, who can enjoy an additional £50 million revenue per season. This is reduced to £30 million after paying the £20 million “mortgage” and clearly the costs of running a bigger operation are higher, but it’s still positive financially with each home game generating around £3.5 million. That is mighty impressive, especially when you consider that Manchester United earn only slightly more per match, even though the capacity at Old Trafford is much higher at 76,000.

Of course, that can also be a double-edged sword, as can be seen in 2010, when the match day revenue fell by £6 million from £100 million to £94 million, because five fewer home games were played. This revenue stream is partly dependent on how far the club progresses in various cup competitions, so even though the derided domestic cups might not contribute much TV revenue, they can still make a difference via good old-fashioned gate receipts.

Despite this drop, Arsenal’s match day revenue is still the second highest in the Money League with most matches selling out. In fact, the club advises us that there is a 40,000 waiting list for season tickets. However, it is difficult to see how they could significantly increase revenue here, as the ticket prices are already among the highest in Europe. Actually, club management has stated that they do not want to raise the cost of admission, which is backed-up by the fact that prices have only been increased once since the new stadium opened.

No, the best hope here is that Arsenal carry on filling the ground, so that current revenue levels of around £100 million can be maintained. This is partly due to what happens on the pitch, as any continued lack of success in terms of winning trophies might adversely affect demand, especially at the premium level, which contributes the most money, but is also the most fickle.

"The match day experience"

Where money has been growing for football clubs everywhere is, of course, television. Many fans could do without the weekly inanities of Messrs. Keys and Gray, but, in fairness, “he who pays the piper, calls the tune” and there is no doubt that Sky pay a pretty penny for their TV rights.

Arsenal’s television revenue increased by 15% from £73 to £85 million in 2010, which was made up of £52 million from the Premier League and £31 million from the Champions League. As a result of finishing third in the Premier League, Arsenal received a higher merit payment, while their facility fees also rose, as they were broadcast live four more times, producing an overall £5 million increase compared to 2009.

The Champions League payout was also higher, even though Arsenal only reached the quarter-finals, as opposed to the semi-finals the previous year. This was due to a number of factors: 2009/10 represented the first year of a new cycle of UEFA broadcasting contracts; additional distribution for the qualifying round; and the weakness of Sterling (Champions League revenue is distributed in Euros). Gazidis has claimed that Arsenal budget so that the club could survive missing a year of Champions league football without selling players, but these figures once again demonstrate the importance of qualification to Europe’s top clubs.

To be fair, Arsenal’s reliance on TV revenue is much less than most other clubs in the Premier League at 38%. Smaller clubs are almost entirely dependent on this revenue stream, hence their narrow ambition of surviving in the Premier League. Relegation really is unthinkable for clubs like Blackburn and Wigan, where TV money accounts for over 70% of their total turnover.

At the other end of the spectrum, the Spanish giants, Real Madrid and Barcelona, are allowed to negotiate individual television deals, so they earn around £50 million a year more than Arsenal. Of course, given the well-publicised problems with Mediapro, their TV partner, and the pressure from other clubs in Spain to move to a collective agreement (as they have just done in Italy), this may be something of a poisoned chalice, but it certainly gives them a competitive advantage for the time being.

Against that, we know that Arsenal will benefit from an increase in Premier League TV revenue next season, as 2010/11 marks the first season of the new three-year deal, which is much higher following the astonishing increase (more than doubled) in overseas rights. The club estimates that this will mean a 10% boost, which would be worth an additional £6 million, but the increase could be as high as £10 million.

Longer-term, their greatest revenue-generating opportunity may come from new media, especially broadcasting live matches over the internet. Working towards that vision, Arsenal Broadband has entered a partnership with the sports media group MP & Silva to develop broadcast and online products aimed at an international audience. There has been concern that some of this opportunity has been lost, as majority shareholder Stan Kroenke bought 50% of Arsenal Broadband, but Chief Commercial Officer Tom Fox has said that this does not include the live rights, which is where the big bucks would be made.

"Captain Fantastic"

Perhaps the greatest disappointment in the accounts was the £4 million decline in commercial revenue to £44 million, which has long been an area of weakness with revenue lagging way behind the club’s English peers. According to the Money League, Arsenal’s annual commercial revenue is much lower than the other teams in the Big Four (Manchester United £70 million, Liverpool £68 million and Chelsea £53 million). The comparisons are even worse against the continental European teams (Bayern Munich £136 million, Real Madrid £119 million and Barcelona £96 million).

Little wonder that the club said, “There is no doubt that the areas of commercial activity and sponsorship provide the greatest opportunity for the Group to generate significant incremental revenues in the medium to long term.” That’s one way of putting it.

Arsenal tied themselves into a long-term deal with Emirates worth a reported £90 million (naming rights until 2021, shirt sponsorship until 2014) in order to provide security for the stadium financing, which made a lot of sense at the time, but recent deals by other clubs highlight the growth opportunity. The amount paid for shirt sponsorship increased this season by £500,000 to £5.5 million, but this pales into insignificance compared to the £20 million Standard Chartered and Aon pay to Liverpool and Manchester United. In fact, five Premier League teams have higher sponsorship deals than Arsenal, even including Spurs, whom nobody would accuse of being the more successful half of North London.

"Ivan Gazidis - you've never had it so good"

The club’s seven-year kit deal with Nike has been extended for a further three seasons to 2014 with the supplier exercising an option in the original agreement. The accounts say that this “delivers an improvement in commercial terms”, but don’t divulge how much it is worth. Given that figures released by Nike and Adidas suggest that only three clubs (Manchester United, Real Madrid and Barcelona) sell more shirts worldwide than Arsenal, the fee paid is almost certainly not enough.

With all the focus on moving to the new stadium, it is clear that commercial opportunities have been put on the back burner, but Ivan Gazidis is well aware of the need for improvement in this area, so he has restructured and strengthened his commercial team to explore new partners and overseas markets. Certainly, they’re well versed in marketing speak: witness Tom Fox’s recent gem when talking to the BBC, “Putting the basic successful product out on the field is a huge component of our brand.” However, it’s now time for them to deliver, starting by applying pressure on Emirates to improve the terms of their deal, if they wish to retain the shirt sponsorship. Arsenal are the biggest team in London, playing in the largest city of Europe, so they have been badly under-sold to date.

The club has invested in a number of overseas developments, including opening retail outlets and soccer schools in the Middle East, Far East and the USA, in order to build its brand internationally, but Gazidis has said that there will be no lucrative pre-season tours to America or Asia until the club has a clear strategy for those regions.

Another revenue stream that is often over-looked for football clubs is the profit made on player sales, which has been very important to Arsenal’s financials in recent years. This was beautifully explained by Peter Hill-Wood, “profits were boosted by some £38 million from the sales of players who were no longer central to his future plans”, in an acidic reference to the transfer of Emmanuel Adebayor and Kolo Toure to the ever-generous Manchester City.

"How much did City pay for me?"

This is nothing new under the sun for Arsenal, as they have averaged £25 million profit on player sales every season since they moved to the Emirates, making good money from stars who were past their sell-by date (Vieira, Henry, Toure) or were disruptive influences in the dressing room (Cashley Cole, Greedybayor).

However, I would suggest that Arsenal cannot rely on Wenger producing the proverbial rabbit from the hat every year and this may not even be desirable. Worryingly, the accounts note, “There has been very limited player sale activity during the summer transfer window. As a result, in contrast to each of the previous three years, we do not have a significant profit on disposal of player registrations on the books at this stage of the new financial year. Subject to any transfer activity in the January 2011 window this may impact the final level of profits to be reported for the financial year 2010/11.” Let’s hope that this does not herald the profitable sale of Cesc Fabregas to Barcelona in a few months.

What is clear is that Arsenal, like other football clubs, will have to work harder for revenue growth in the future, as TV cannot be relied upon to continue its vertiginous growth in perpetuity. Tom Fox posed the question, “In five to ten years’ time, we are going to have to ask: where are we going to grow our business?”

On the cost side, wages have risen 6% to £111 million, which is partly “driven by the external environment in which we operate where player costs continue to go up” (according to Gazidis), but largely reflects the re-signing of many players on long-term contracts, which represents “the best means of protecting the value of one of our most important assets” (according to Hill-Wood).

Despite the increase, the wage bill is still substantially below Manchester United (£123 million) and Chelsea (£149 million), but in fairness it’s considerably more than the payrolls of the chasing pack: Liverpool £90 million, Aston Villa £61 million and Tottenham £59 million. I have excluded Manchester City, as I confidently expect their wage bill to have shot up to around £125 million in their next set of accounts.

Having said that, Arsenal have admitted that “there is strong upward pressure on player wages”, so “wage costs for 2010/11 will show a significant increase”, as the full impact of revised contracts signed in the last 18 months comes through. Of course, these are not just player salaries, as they also include the strengthening of the executive team, which must come at a price, though theoretically should also increase revenue.

After falling for three years, the wages to turnover ratio has increased (deteriorated) this year to 50%, though this is still very respectable and remains the second best in the Premier League. In fact, only five teams have a ratio below 60%, while six teams are working with a completely unsustainable ratio above 90%.

What does seem very high at Arsenal is the £55 million for “other operating costs”, i.e. excluding salaries, depreciation and amortisation, which is actually higher than the total costs at seven Premier League clubs. Unfortunately, the club does not provide much detail for these costs, but they must include items like stadium operating costs, utilities, retail expenses and travel. What we can see is that these costs represent 25% of football turnover, which seems ripe for a spot of judicious cost cutting.

On the other hand, player amortisation, namely the annual cost of writing down the cost of buying new players, is very low at £25 million, barely changed from the year before. As you would expect, it’s much higher at those clubs that have pursued success via the cheque book, in fact over twice as much: Barcelona £61 million, Real Madrid £55 million and Chelsea £49 million.

This reflects Arsenal’s policy of not venturing too often into the transfer market, even though ample funds are available, which was epitomised by the short list of names purchased this summer: Marouane Chamakh from Bordeaux, Laurent Koscielny from Lorient and Sebastien Squillaci from Sevilla.

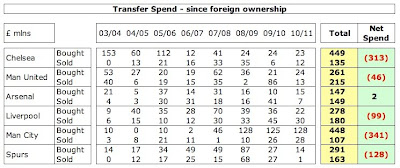

In fact, the Gunners have consistently spent less than their rivals over the last few years in the transfer market. Since the arrival of Roman Abramovich, Arsenal is the only top club to make money from buying and selling players with a small surplus of £2 million. Although reported transfer fees are notoriously unreliable, it is beyond dispute that other clubs’ net spend is significantly higher: Manchester City £341 million, Chelsea £313 million, Liverpool £99 million and Manchester United £46 million (boosted by the amazing Ronaldo profit).

Arsene Wenger has steadfastly refused to endanger Arsenal’s financial security by splashing out large sums on over-priced, big name players. For Arsenal to spend not just less, but so much less than these clubs and still challenge for honours is testament to the incredible job that Wenger has done with the funds available.

Equally remarkable are the results from the property side of the business, which generated £157 million of revenue from the sale of 362 apartments at Highbury Square (£134 million) and social housing at Queensland Road (£23 million), leaving the property business debt-free. This represents a remarkable turnaround from a year ago, when the downturn in the property market forced the club to extend the repayment deadline on the bank loan from April to December (at higher rates of interest), to reflect delays in sales completion.

"Chamakh attack"

At the time the books were closed, 570 of the 655 apartments at Highbury Square had been sold, leaving only 85 still available. Gazidis has since informed us that the 600th sale was completed in August with the remainder expected to be sold in the next accounting year. Based on the average price of sales to date of around £400k, that would produce proceeds of £34 million. As the loans have now been paid off, all of this is surplus cash that will be available to spend.

It’s a similar story for the club’s other property developments (“in-fill” sites at Highbury Square, Hornsey Road, Holloway Road and Market housing at Queensland Road), though it’s much more difficult to estimate what these would be worth. In any case, any proceeds here are unlikely to reach completion before 2011/12. This will obviously produce some cash, but let’s hope that it’s not too much of a distraction for management before the club finally exits the property business.

Following the elimination of the property debt, the club has managed to reduce its gross debt to £263 million, leaving just the long-term bonds that represent the “mortgage” on the Emirates Stadium (£237 million) and the debentures held by supporters (£27 million). Once cash balances of £128 million are deducted, net debt is down to only £136 million, which is a significant reduction from the £298 million the previous year. The club expected the debt to peak in 2008, which it did, but it is now back down to levels last seen in 2004.

This is in stark contrast to the debt held by the other top clubs in the Premier League, which is not only much larger, but continues to rise. A year ago, Manchester United’s debt stood at £566 million (gross £716 million), but the accumulating interest on their PIK loans (now at an eye-watering 16.25%) will surely have increased that figure. Similarly, Liverpool’s net debt of £351 million has been attracting punitive penalty payments for months.

It is the huge interest payments that wreck the business model of these clubs (£69 million for Manchester United and £40 million for Liverpool), which is considerably higher than the £20 million that Arsenal pay to service their loans (£15 million interest, £5 million capital repayment).

It’s not clear whether it would be possible for Arsenal to pay off the outstanding debt early in order to reduce the interest charges, but my guess is that they are in no hurry to do so, as Gazidis has argued that not all debt is bad, “The debt that we’re left with is what I would call ‘healthy debt’ – it’s long term, low rates and very affordable for the club.” In any case, the accounts clearly state, “Further significant falls in debt are unlikely in the foreseeable future. The stadium finance bonds have a fixed repayment profile over the next 21 years and we currently expect to make repayments of debt in accordance with that profile.”

The press release did not fully analyse creditors, so we do not know how much Arsenal owe other football clubs for transfers. As an indicator, last year other creditors included £26 million for such debts. To balance that, the 2009 accounts also included £23 million outstanding payments from other clubs in other debtors, so the net position was negligible.

"Two arguments to spend"

Included within the net debt are astounding cash balances of £128 million, though the club is keen to emphasise the seasonal nature of cash flows, i.e. money taken from season ticket renewals will be used to pay operational expenses over the next few months. Furthermore, the club has to hold £38 million as reserves (£31 million as security for the bonds and £7 million for Queensland Road property development). However, that still leaves £90 million of available cash in the pot.

This begs the obvious question of why has Wenger been so reluctant to spend? There is no doubt that the move to the new stadium limited Arsenal’s transfer budget over the past few years, but the financial situation has greatly improved and it is clear that funds are available to buy the players that the team needs. However, there is still a suspicion that the manager would prefer to build rather than buy, so much of the low spending is out of choice. Indeed, Gazidis clarified the club’s stance last year, “We believe transfer spending is the last resort. That’s a sensible view to have. Re-signing players is a far more efficient system.”

Wenger is clearly singing from the same song sheet, as he has reiterated his preference for developing young players to dipping into the transfer market, “If I go out and buy players, then Jack Wilshere doesn’t come through.” He gave a further insight into his thoughts, when he argued, “The job of a manager is not to spend as much money as possible.”

That must be music to the ears of the board, whose chairman again spoke of their “commitment to a financially self-sustaining business model.” This is a tricky target at the best of times, but very difficult to maintain when you’re competing against billionaires for whom money is no object or clubs who appear to have decided that it does not matter if they don’t have any money, opting to build up substantial debt instead. In fact, Gazidis has admitted that the club can’t “compete with Manchester City in the transfer market, because those kinds of fees and salaries are unsustainable for any football business.”

"Jack the lad"

However, the football world is changing with the advent of the UEFA Financial Fair Play regulations meaning that the era of the big spender may be drawing to an end. Many top clubs, including Chelsea, have already visibly cut back on their spending, while others will need to put their house in order if they wish to compete in Europe. Arsenal will have no problem complying with the new rules, but other clubs will have to adopt a similar model to avoid making losses – unless their accountants and lawyers succeed in locating some convenient loopholes.

That’s all very well, but fans of those other clubs can bask in the reflected glory of the silverware that they’ve won, while Arsenal can only boast of the winning the league of balance sheets (which doesn’t actually exist, if you’re wondering). Gazidis has stressed that “trophies are our main objective and ambition”, but he slightly ruined this determined stance, when he added, “If we can’t win trophies, qualifying for the Champions League is the base line.”

In fairness, it is an incredible achievement for any team to gain qualification for the Champions League 13 years in a row, as Arsenal have done, especially when battling against the financial constraints imposed when building a new, state-of-the-art stadium. Arsene Wenger deserves many plaudits for the minor miracle he has performed over the last few years: guiding the club through the substantial upheaval of leaving its spiritual home of Highbury for the Emirates; developing a squad of exciting young players; and yet still keeping the team competitive, all the while playing the most attractive football in the country.

"What more can I do?"

However, his reign has been a little like the proverbial “game of two halves”, winning three Premier League titles and four FA Cups in his first nine years, followed by no trophies at all in the last five years, which has provoked impatience among some supporters and a growing lack of understanding over the unwillingness to buy world-class players. There is no doubt that he is an outstanding manager, though there is a feeling that he might need to modify his transfer policy and loosen the purse strings to ensure that his legacy is not tarnished.

Swedish legends ABBA managed to capture the fans’ feelings quite well in one of their classic hits, “Money, money, money/Must be funny/In the rich man’s world”, Yes, indeed. Have you heard the one about the football club that made over £60 million profits, but couldn’t afford a decent goalkeeper?

{kind=link}

{kind=link}